View/Download this article in PDF format.

The federal coal program has been repeatedly criticized by offices like the Government Accountability Office [1] and the Inspector General at the Department of Interior (DOI) for failing to capture a fair return for taxpayers. Interior’s Bureau of Land Management (BLM) is responsible for managing this program. In fiscal year 2012, coal tracts leased under the federal coal leasing program accounted for about 42 percent of the 1.05 billion tons of coal produced in the United States.

Under the Mineral Leasing Act, the minimum royalty for coal produced from federal leases is 12.5 percent, though a lower rate may apply to underground coal mining. The BLM currently sets the royalty rate for surface mining at 12.5 percent and the rate for underground mining at 8 percent. [4] However, under provisions of the law BLM has broad discretion to reduce this royalty rate. The royalty reductions are based on financial data provided by the lessee, and in no case may royalty rates go below 2 percent.

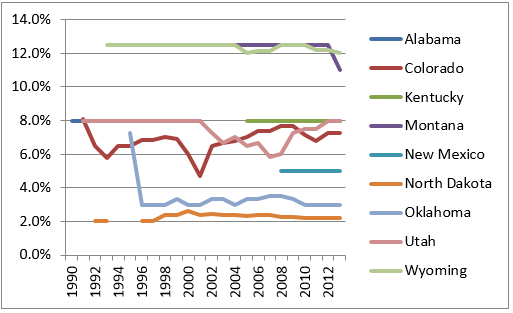

Average Royalty Rate by State, 1990 – 2013

According to data obtained from the Office of Natural Resource Revenues (ONRR), which manages the annual revenues from federal energy and mineral leases, BLM has reduced the royalty rates on federal coal leases frequently during the last 25 years. Of 80 federal leases in nine states, 35 of them (44 percent) recorded royalty rates less than the minimum of 12.5 percent for surface mines and 8 percent for underground mines. More than half (16 of 28) of the royalty rate reductions occurred between 2001 and 2007. Among the standouts are:

- North Dakota: All 11 federal leases in ND of different durations beginning in 1992 through 2013 received a royalty rate reduction. The average royalty rate for all 11 leases was 2.33 percent.

- Oklahoma: All six federal coal leases in OK of different durations received a royalty rate reduction, paying an average royalty rate of 3.39 percent on federal coal beginning in 1995 through 2013. One OK lease received a rate reduction of 10.5 percent (from 12.5 percent to 2.0 percent) in 1995, remaining at 2.00 percent through 2013.

- Colorado: 11 of the 19 federal coal leases in CO received at least one reduction in royalty rate during the period from 1992 through 2013.

The loss in federal revenue from these royalty rate reductions cannot be calculated from this data because the volume of coal extracted from the individual leases or the relative amount of coal produced on leases with reduced royalty rates is not currently publicly disclosed. In a separate analysis of BLM data, Headwaters Economics estimated that royalty rate reductions have reduced total royalty payments by roughly $294 million on all leases sold between 1990 and 2013. Headwaters notes that these leases only account for roughly one-third of the amount of coal produced during this period, and that the remainder is from leases sold prior to 1990. If losses from royalty rate reductions are consistent with older leases, the total cost of reduced royalty rates is “closer to $860 million from 1990 to 2013, or about $37 million annually (in 2013 dollars).” [6]

Recommendations

The discretion to reduce royalty rates was granted as part of the Federal Coal Leasing Amendments Act of 1976 (FCLAA) because the legislation represented a significant increase in royalties at the time. Decades later, the justification for the royalty rate reductions no longer exists – the baseline rates have been in effect for almost 40 years and apply to many existing leases. Fairness to both taxpayers and industry competitors requires that the royalty rate be made consistent for all lessees.

At a minimum, BLM could improve transparency by collecting data from the field on a monthly basis. Each month, each state office should report the number of royalty rate reduction requests they have received, the number of requests they have granted and the justifications therefor, the volume anticipated to be valued at the reduced rate. These aggregate numbers would not disclose any confidential data about individual mines, which BLM has been reluctant to disclose due to lessees’ concerns about trade secrets.

Thus, there is no reason BLM should not make this data publicly available on its website. Data of this nature would provide an essential baseline for understanding the impact of royalty rate reductions upon taxpayer receipts, and would be consistent with the Department of the Interior’s Extractive Industries Transparency Initiative. The impact of policy decisions regarding rate reductions could then be evaluated based on openly available data.