Seeing as April 15th is right around the corner, we’ll keep the tax reform ball rolling this week. As promised, Ways and Means Committee Chair Dave Camp (R-MI) began a series of hearings in the House this week on so-called tax extenders, the laundry list of “temporary” tax breaks Congress repeatedly extends to avoid the more difficult work of reforming the tax code. After much sound and fury in their opening statements, the Senate Finance Committee passed their bill last week without much reform – cutting a couple, adding a couple. Rep. Camp has promised to debate necessity of continuing these tax breaks, many of which are just corporate welfare.

Here’s our contribution to the debate. Instead of extending (again) these expiring provisions, we’d like to see the Committee take up the comprehensive tax reform proposals introduced by Chairman Camp and former Senate Finance Committee Chairman Max Baucus (D-MT). We can’t keep doing the same thing and expect a different result. Instead of rubber-stamping special carve-outs in the tax code for another two years, Congress should start making some decisions.

Temporary tax extenders and the broader universe of tax expenditures – the permanent breaks, deductions, and credits for specific activities like home mortgage interest or charitable giving – cost nearly $1.1 trillion every year. They’re like a mirror image of discretionary spending. But unlike the scorn that is heaped upon federal spending each year (some of which is with good reason), there seems to be a chorus of excuses when it comes to special tax breaks. It’s a double standard. And it shows: not just in the continuing absurdity of the tax extenders process, but in the effective tax rates of some of the biggest beneficiaries of tax subsidies in general.

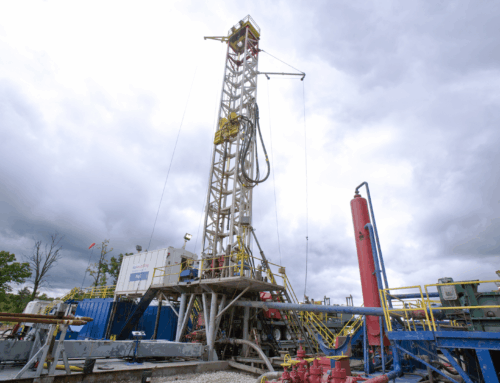

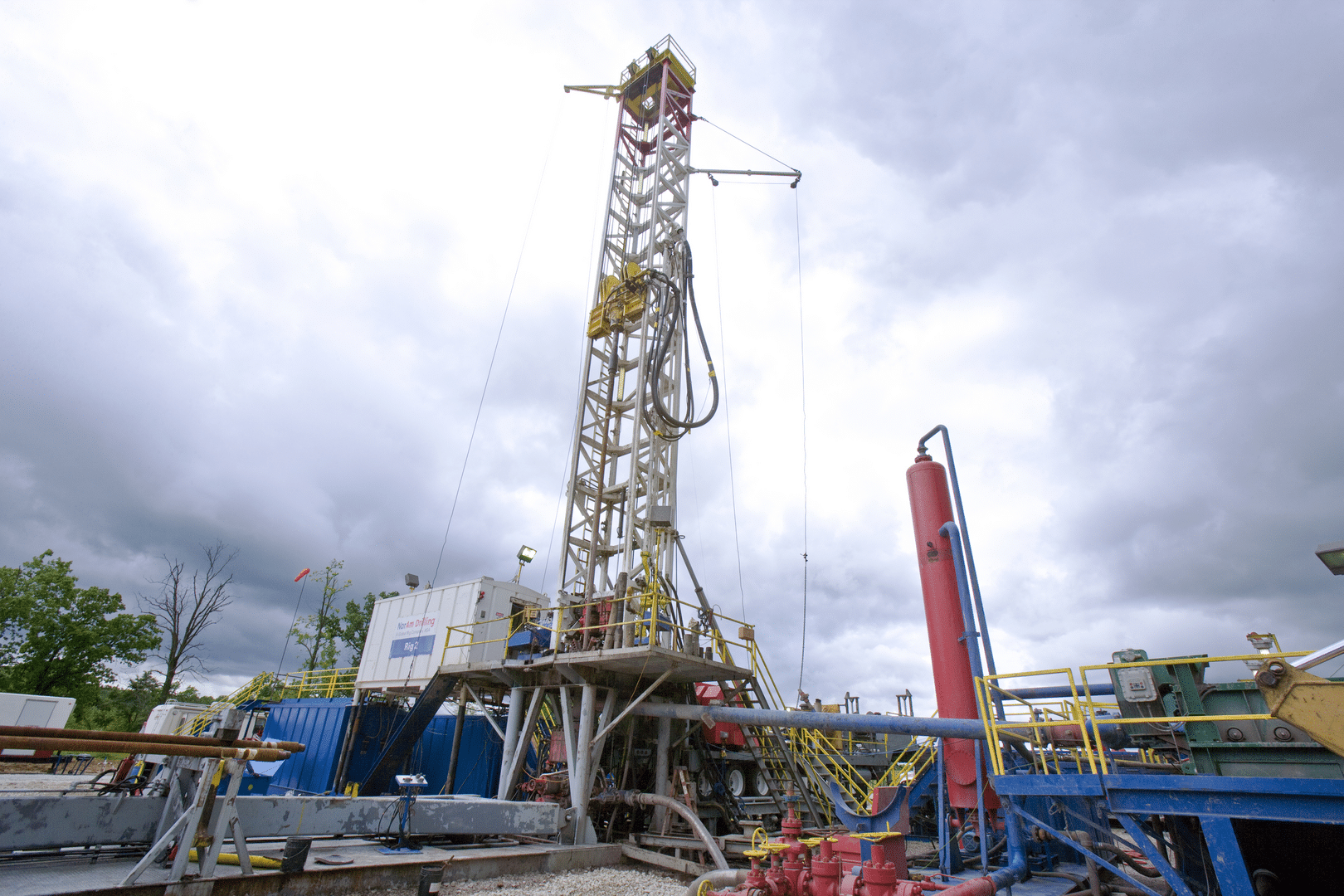

This week, we released our analysis of tax subsidies that benefit the oil and gas industry. We consider the oil and gas industry a good example of taxpayers that don’t need subsidies, through direct spending or the tax code, because the industry has been subsidized for a hundred years (literally) and it is one of the most profitable in the world (literally). We found that the three largest U.S.-based oil and gas companies had an average U.S. tax rate of 26.2 percent for 2008-2012. If you subtract the billions the companies are allowed to defer each year (thanks to these special tax provisions), it drops to around 20 percent. And, to be sure, oil and gas companies are not the only ones picking from the menu of various tax subsidies to lower their rate below the statutory rate of 35 percent.

The same holds true for individual taxpayers. Special tax deductions that have been in effect for decades benefit a small slice of taxpayers, but cost everyone. Even popular ones like the mortgage interest deduction, which costs roughly $75 billion a year, have no effect on homeownership rates in this country and are basically offset by the increase in home prices it causes. Like the oil and gas industry, some of the wealthiest individual taxpayers can avoid paying higher rates by also utilizing special tax provisions that aren’t available to everyone.

Congress could lower overall tax rates – something everyone wants to do – by cutting out the whole thicket of special credits and deductions that distort both the tax system and business decisions. So why don’t they just do it already? Because when it comes time to cut someone’s special tax perk, which may have been on the books for decades (regardless of its efficacy), everyone runs for the exit. Witness last week’s vote in the Senate Finance Committee, or the full-throated defense of bad tax policy like last-in, first-out accounting, which relies on demonstrably false assumptions about company inventories. This is why it has been more than 30 years since Congress reformed the tax code. And until Congress (and the rest of us) start treating spending through the tax code the same as regular government spending, the tax code will continue to be an embarrassing source of government waste.