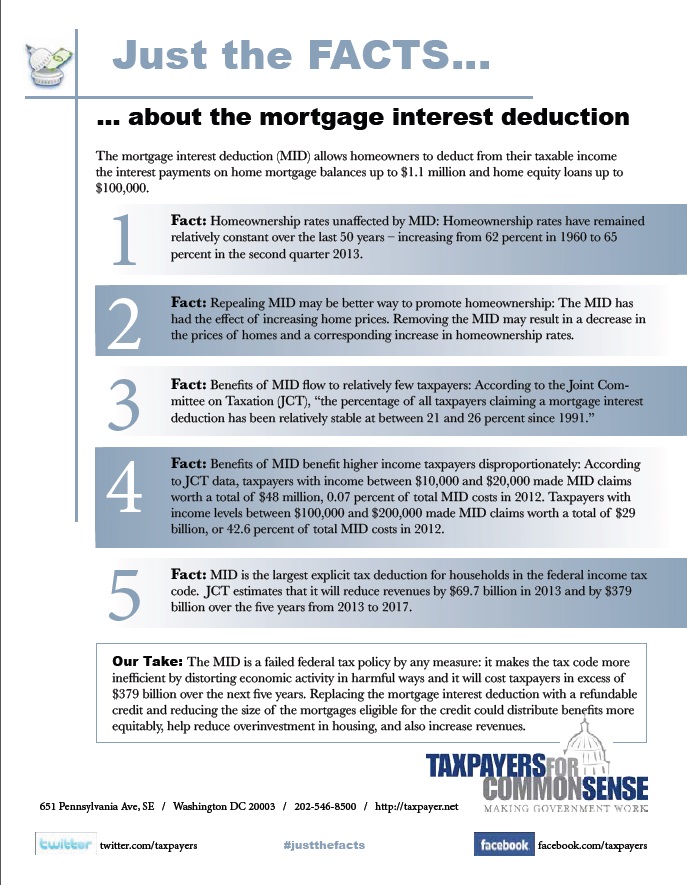

The mortgage interest deduction (MID) allows homeowners to deduct from their taxable income the interest payments on home mortgage balances up to $1.1 million and home equity loans up to $100,000. The MID is a failed federal tax policy by any measure: it makes the tax code more inefficient by distorting economic activity in harmful ways and it will cost taxpayers in excess of $379 billion over the next five years.

Background

The MID was not designed to promote homeownership. In 1913, the first year tax forms were issued by the Internal Revenue Service (IRS), the tax code allowed for the deduction of all interest. With such a high personal exemption (equivalent to $70,000 today),[1] very few taxpayers used the MID. Not until World War II, when Congress lowered exemptions and raised tax rates, did the MID become a significant deduction. During the baby-boom years, the MID may have helped drive the increase in homeownership rates from 44 percent in 1940 to 62 percent in 1960. The last major reform to the MID was during the 1986 tax reform under President Ronald Reagan, when the amount of the deduction was limited to its current level.

Evidence against the MID

There is a wealth of data that shows the MID is costly and counter-productive, including the following:

-

Homeownership rates are unaffected by MID: Homeownership rates have remained relatively constant over the last 50 years – increasing from 62 percent in 1960 to 65 percent in the second quarter 2013.[2] According to Harvard economists Edward L. Glaeser and Jesse M. Shapiro: “The irrelevance of the deduction is supported by the time series, which shows that the ownership subsidy moves with inflation and has changed significantly between 1965 and today, but the homeownership rate has been essentially constant.”[3]

-

Repealing MID may be better way to promote homeownership: The MID has had the effect of increasing home prices. The market has essentially internalized the savings the MID offers to potential homeowners. Removing the MID may result in a decrease in the prices of homes and a corresponding increase in homeownership rates. Using an international sample of housing prices in countries with the MID and countries without an equivalent deduction, one study found: “the U.S. empirical literature shows that, while the MID can lower the user cost of housing, the tax savings are capitalized into house prices… Thus, the removal of the MID would lower house prices… sufficiently to increase homeownership.”[4]

-

Benefits of MID flow to relatively few taxpayers: Because the MID is an itemized deduction, it is only available to taxpayers who itemize their deduction rather than taking the standard deduction. The percentage of taxpayers who itemize their deductions can range from roughly 19 percent in West Virginia to 48 percent in Maryland.[5] In 2009, only about one-third of taxpayers nationwide filed itemized deductions and only about one-quarter claimed the MID.[6] According to the Joint Committee on Taxation (JCT), “the percentage of all taxpayers claiming a mortgage interest deduction has been relatively stable at between 21 and 26 percent since 1991.”[7]

-

Benefits of MID benefit higher income taxpayers disproportionately: Not only do the benefits of the MID flow to relatively few taxpayers, but also the overwhelming amount of the benefits of the MID go to wealthy taxpayers, most of whom would likely own homes with or without the MID. According to JCT data, taxpayers with income between $10,000 and $20,000 made MID claims worth a total of $48 million, 0.07 percent of total MID costs in 2012. Taxpayers with income levels between $100,000 and $200,000 made MID claims worth a total of $29 billion, or 42.6 percent of total MID costs in 2012.[8]

-

MID distorts investment decisions in unproductive ways: MID has resulted in overinvestment in housing in the U.S. Repeal of the MID and reallocation of those resources could boost economic growth. According to the Federal Reserve Bank of Dallas: “the unmeasured benefit to housing investment would have to top $220 billion per year (or $300 per month for each owner-occupied home) to support the current allocation of resources. Absent such large unmeasured benefits from investment in housing, the evidence suggests the U.S. economy could grow faster if society shifted more of its resources away from housing and into high school education and, especially, nonhousing fixed capital.”[9]

-

MID promotes risky levels of household debt: The financial crisis of 2008 was largely the result of over-indebtedness of residential homebuyers. Because the benefits of the MID flow mostly to the upper-income tiers, its effect has been to encourage purchase of larger homes and excessive housing debt. “As we know, a crucial problem has been that many homeowners found themselves ’under water‘ as the value of their homes fell below the balance of their mortgages. A key contributor to excessive housing debt is the deductibility of home equity loans that can be used for personal consumption.”[10] The MID has also encouraged the purchase of homes through debt rather than with assets. Taxpayers with income between $125,000 and $250,000 hold non-housing, non-retirement assets worth 63.5 percent of their mortgage debt that might be used to finance mortgages absent the MID.[11]

- MID is expensive to maintain: MID is the largest explicit tax deduction for households in the federal income tax code. JCT estimates that it will reduce revenues by $69.7 billion in 2013 and by $379 billion over the five years from 2013 to 2017.[12]

Conclusion

The long-standing argument against reform or repeal of the MID in spite of all the evidence of its failure has been the popularity of the deduction among voters. Congress can reform MID in ways that will soften the political fallout and the impact on the housing market. One option discussed at length in a variety of papers is the replacement of the MID with a tax credit. One proposal to replace the mortgage interest deduction with a 15 percent refundable credit and reduce the size of the mortgages eligible for the credit could distribute benefits more equitably, help reduce overinvestment in housing, and also increase revenues by approximately $300 billion.[13]

[1] Bruce Bartlett, “The Sacrosanct Mortgage Interest Deduction,” The New York Times (6 August 2013): http://economix.blogs.nytimes.com/2013/08/06/the-sacrosanct-mortgage-interest-deduction

[2] U.S. Department Of Commerce, U.S. Census Bureau, “Residential Vacancies And Homeownership In The Second Quarter 2013” (July 30, 2013): http://www.census.gov/housing/hvs/files/currenthvspress.pdf

[3] Edward L. Glaeser, Jesse M. Shapiro, “The Benefits of the Home Mortgage Interest Deduction” (January 2003): http://www.nber.org/chapters/c11534

[4] Steven C. Bourassa, Donald R. Haurin, Patric H. Hendershott, Martin Hoesli, “Mortgage Interest Deductions and Homeownership: An International Survey,” Swiss Finance Institute Research Paper No. 12-06 (March 13, 2013)

[5] Nick Kasprak, “Weekly Map: Who Itemizes?” Tax Foundation (May 15, 2013): http://taxfoundation.org/blog/weekly-map-who-itemizes

[6] Dean Stansel and Anthony Randazzo, “Unmasking the Mortgage Interest Deduction: Who Benefits and by How Much?” Reason Foundation, Policy Study 394 (July 2011): http://reason.org/files/mortgage_interest_deduction.pdf

[7] U.S. Census Bureau, Homeownership Rates (1994 to 2010): www.census.gov/hhes/www/housing/hvs/qtr410/files/tab5.xls

[8] Congress, Joint Committee on Taxation, “Estimates Of Federal Tax Expenditures For Fiscal Years 2012-2017, February 01, 2013: Table 3.–Distribution by Income Class of Selected Individual Tax Expenditure Items, at 2012 Rates and 2012 Income Levels”: https://www.jct.gov/publications.html?func=startdown&id=4503

[9] Lori L. Taylor, “Does the United States Still Overinvest In Housing?” Federal Reserve Bank Of Dallas Economic Review Second Quarter 1998: https://www.dallasfed.org/assets/documents/research/er/1998/er9802b.pdf

[10] Op. cit., Bartlett

[11] James M. Poterba, Todd M. Sinai, “Income Tax Provisions Affecting Owner-Occupied Housing: Revenue Costs And Incentive Effects” National Bureau Of Economic Research, Working Paper 14253, Table 6: Fraction Of Outstanding Deductible Mortgage Debt That Homeowners Could Replace By Liquidating Other Assets, By Household Age And Income: Http://Www.Nber.Org/Papers/W14253

[12] Congress, Joint Committee on Taxation, “Estimates Of Federal Tax Expenditures For Fiscal Years 2012-2017, February 01, 2013: Table 1.–Tax Expenditure Estimates By Budget Function, Fiscal Years 2012 – 2017”

[13] Alan D. Viard, “Replacing the home mortgage interest deduction,” American Enterprise Institute, The Hamilton Project (February 26, 2013): http://www.aei.org/files/2013/02/26/-replacing-the-home-mortgage-interest-deduction_093929900894.pdf