Over the years, taxpayers have lost big from the sale of federal assets, including natural resources like oil, gas, coal, and timber. The government sells leases for federal lands and waters so that private industries can extract, drill, and harvest these valuable resources. And there is nothing wrong with that. But when the feds fall asleep at the wheel, taxpayers are hit when the receipts crash.

One of the problems we have talked about before is the federal government’s inability to keep up with the market, and the cost this can have for taxpayers. One example is this year’s sale of offshore oil and gas leases in the western Gulf of Mexico. The Bureau of Offshore Energy Management (BOEM) recently issued its annual press release declaring that the lease sale had garnered $22.7 million in high bids for the Treasury. There’s just one problem: this is far less than what the feds received for previous sales, as the number of leases and the prices paid have dropped off sharply.

In 2014, the western Gulf of Mexico lease sale brought in $110 million for 81 leases. In 2013, the total was $102 million for 53 tracts. This year, it was $22.7 million for only 33 tracts. The drop in price per tract is dramatic; a little math shows this year’s average price for each potential lease (less than $700,000 per sale) is about half of last year’s average winning bid ($1.4 million per sale) and nearly a third during the year before ($1.9 million per sale). Not surprisingly, the low price correlates with a lack of competition – none of these sales had more than one bidder – there were 33 separate bids for 33 separate tracts.

This is a familiar story. Secretary Jewell recently alluded to similarly low bids for federal coal in a speech, saying: “I think most Americans would be surprised to know that coal companies can make a winning bid for about a dollar a ton to mine taxpayer-owned coal.” The Bureau of Land Management (BLM) has long been criticized for non-competitive lease sales for federal coal; BOEM is not the only one.

On its website, BLM provides some information about 105 separate coal lease sales from 1991 to 2014, almost half of them in Wyoming and Colorado. Combined, all of these sales account for 8.9 billion tons of minable federal coal. The successful bids for these leases, many of which were the only bids, averaged $0.38 per ton. One company – Coteau Properties Co. (part of the North American Coal Corporation) – has leases accounting for 116 million tons of federal coal, for which it successfully bid an average of a penny per ton. Coteau’s bids make Secretary Jewell’s example look generous. In addition, the aggregate number of lease sales has also declined in recent years, with only two lease sales in 2014 and one in 2013.

The most likely causes for the loss of interest in offshore oil leases are obvious – the price of oil has dropped dramatically, and domestic onshore gas production has increased substantially, leading the oil and gas companies to invest less in new offshore supply. Similarly, the price of coal has also come under pressure from the sharp increase in cheap natural gas. This has caused a drop in demand for coal as baseload power generation has shifted from coal plants to gas-fired plants.

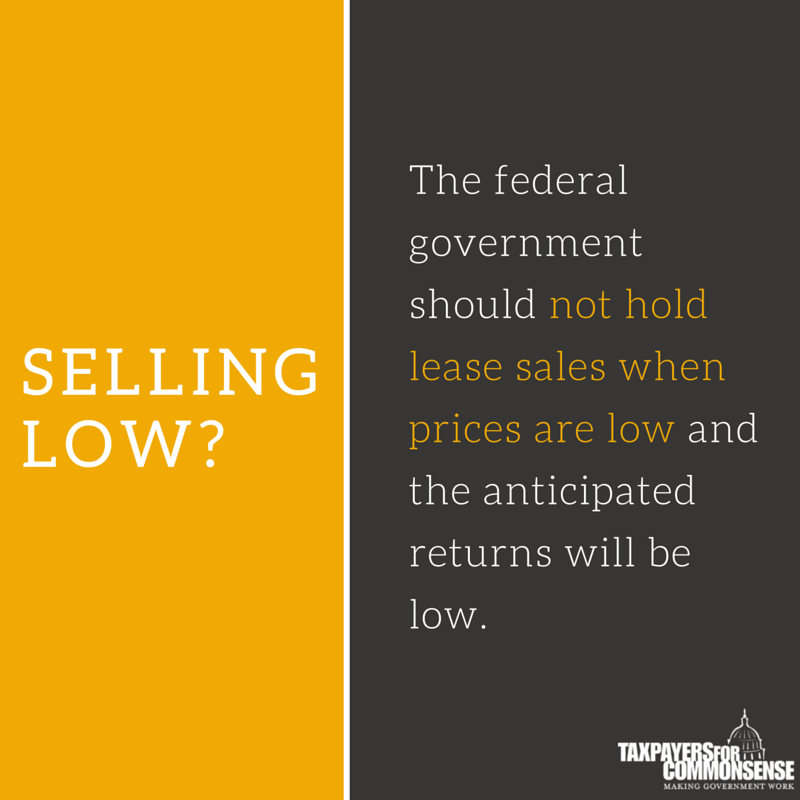

Cheap natural gas is crowding out oil and coal, but the federal government keeps selling leases even as prices continue to drop. The federal government should not hold lease sales when prices – and the anticipated returns – are so low. Rather, the lease sales should be delayed until market conditions suggest the sales will yield the best return to taxpayers. Instead, the feds are acting like the mortgage is underwater and we need to do a short sale to unload these properties. The market has spoken, and just as any private landowner would avoid selling when prices are so low, so too should the feds.