Please find our updated fact sheet here.

In February 2010, the Department of Energy (DOE) conditionally offered Southern Company and its partners a total of $8.33 billion in taxpayer-backed loan guarantees[1] to build two nuclear reactors in Georgia, but the award has yet to be finalized. According to documents obtained through the Freedom of Information Act, the Department of Energy and project partners have struggled to reach an agreement on an appropriate credit subsidy cost for the loan guarantee. Southern Company and partners have now spent four years lobbying policymakers to craft a deal that heavily benefits them and exposes U.S. taxpayers to even greater risk.

While Southern Company and its partners push for increasing reliance on taxpayers, the construction of Plant Vogtle reactors 3&4 has experienced substantial cost overruns and schedule delays. Subsequently, each of the project owners’ credit ratings has been downgraded or their credit outlook changed to ‘Negative’ by one of the top financial ratings agencies.[2]

If the loan guarantee is finalized, the subsidy would be provided through the same program that awarded more than $500 million to the now-defunct solar power company, Solyndra.

A Project in Trouble

In 2008, Southern Co. and its utility partners[3] applied to receive a federal loan guarantee to construct two 1,100 MW Westinghouse AP1000 reactors (reactors 3&4) at Southern Co.’s Plant Vogtle near Waynesboro, Georgia. Southern Co. experienced massive cost overruns while constructing the first two reactors at the site in the 1980s. Original estimates for Vogtle reactors 1&2 were under $1 billion each, but final costs skyrocketed to nearly $9 billion.

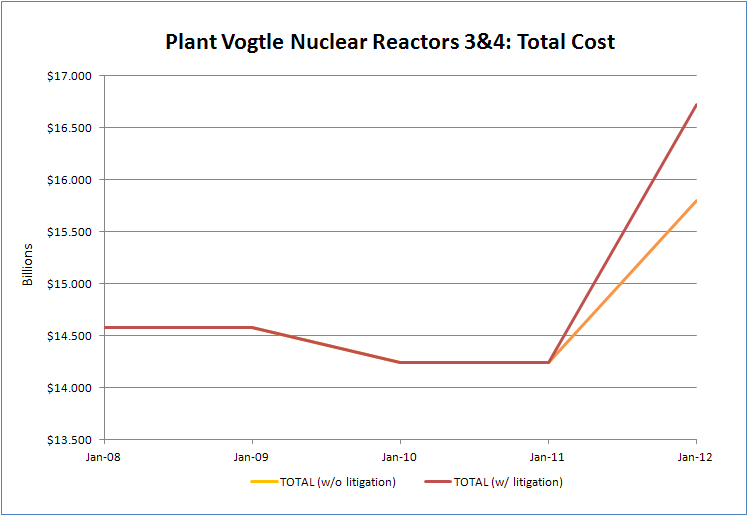

Project Cost

Project Cost

In August 2008, it was originally estimated that Plant Vogtle reactors 3&4 would cost $14.3 billion and begin commercial operations in 2016 and 2017 respectively. Today, the estimate of the project’s cost has reached $15.5 billion and the reactors are projected to come online in 2018 and 2019 respectively. Pending lawsuits between project partners and the construction contractors could push the project’s final costs even higher to $16.5 billion.

- In a February 2013 report to the Georgia Public Service Commission (PSC), Georgia Power (subsidiary of the Southern Company) requested approval of cost overruns totaling $737 million, signifying an increase of the initial $14.3 billion cost estimate to $15.5 billion (an 8.4 percent increase).

- Westinghouse and the Shaw Group (recently purchased by Chicago Bridge and Iron)—the two contractors hired to construct Southern’s two new units— filed suit against Southern Co. and its partners in 2012 seeking around $900 million for the costs of construction design changes. As of February 2014, litigation is pending as interest continues to accrue on the disputed costs which have risen above $930 million. If the project partners lose the lawsuit, total costs of the project could rise to $16.5 billion (14.9 percent more than initial cost estimates).

Project Delays

In August 2008, the initial construction schedule projected that Plant Vogtle reactors 3&4 would reach commercial operation in 2016 and 2017. Since then, Southern Company and its partners have failed to meet many of the project construction deadlines. Today, the reactors are projected to be completed in 2018 and 2019.

- The type of reactor, the Westinghouse AP1000, has never been built in the U.S. before or ever successfully completed anywhere in the world. Reactor design approval took five years and 19 alterations to meet basic safety requirements set by the U.S. Nuclear Regulatory Commission (NRC).

- In June 2011, the PSC-hired Independent Construction Monitor testified that the construction of Plant Vogtle reactors 3&4 was two months behind schedule. A few months later, the project fell to five months behind schedule.

- In April 2012, NRC inspectors reported that the rebar in the “basemat,” or the foundation, for reactor three had been improperly installed. A proposal to compensate for the faulty rebar and correct foundation unevenness was finally approved by the NRC in October, allowing work to resume on the area after six months of costly delay.

- The Shaw Group—recently purchased by Chicago Bridge and Iron—is responsible for the assembly of many of the key reactor components in Lake Charles, LA. Once assembled, components are transported to Georgia for final assembly. An independent monitor reported in Dec., 2012 that The Shaw Group “clearly lacked experience in the nuclear power industry and was not prepared for the rigor and attention to detail required to successfully manufacture nuclear components.” In the period from July 2012 – December 2012, the project contractors were forced to repair “welds on [reactor components] that were found to be the wrong type of weld” according to the most recent IM report. Additionally, an oversized 300-ton reactor vessel nearly fell off the transport train while on route to Plant Vogtle. The reactor vessel was returned to the Port of Savannah where it sat for nearly a month before eventually making its way to the site. By December 2012, the project was more than a year behind schedule.

- In an August 2013 report, the independent monitor stated that the construction contractors have “not demonstrated the ability to fabricate high-quality CA20 submodules at its Lake Charles, La., facility that meet the design requirements at a rate necessary to support the project schedule.”

- In his most recent testimony before the PSC in July 2013, the IM projected that the project is now 21 months behind schedule with final commercial operation dates for Plant Vogtle reactors 3&4 in early 2018 and 2019.

Loan Guarantee Going to Unstable Partners

As a result of the escalating construction costs and continued delays of the Plant Vogtle project, financial rating agencies are downgrading their assessment of the partners involved in the project:

- Standard and Poor’s downgraded the Outlook on Southern Company and Georgia Power’s credit ratings from ‘Stable’ to ‘Negative’ in May, 2013.

- Fitch Ratings downgraded the outlook on all of Oglethorpe Power Corporation’s bonds from ‘Stable’ to ‘Negative’ in August, 2013.

- Moody’s has downgraded the outlook on Municipal Electric Authority of Georgia bonds from ‘Stable’ to ‘Negative.’

- Goldman Sachs and Zacks Investment Research have rated Southern Company as a “sell.” Golden Sachs cited “accelerating capital spending on Vogtle nuclear project and ongoing litigation with the plant’s contractors” as well as the Kemper coal gasification plant and a GA Power rate case that has since resulted in a disappointing ruling for the company. Zacks pointed to weak share earnings, increased expenses, and high risks associated with the construction of reactors 3 and 4 at Plant Vogtle. With the likelihood of additional delays and cost overruns, Zacks states “the project cost could easily end up around $20 billion.”

| Jeffries LLC on 6/17/2013: Southern Company stock rating is downgraded from ‘Buy’ to ‘Hold’ (6/17/13) | Goldman Sachs: Southern Company stock rating is downgraded from ‘Hold’ to ‘Sell’ (4/24/13) | Zack’s Investment Research: Southern Company stock rating is downgraded from ‘Hold’ to ‘Sell’ (6/20/13) |

For more information on the Plant Vogtle project partners see Appendix One.

Seven Extensions – DOE Dangling Massive Subsidy

DOE conditionally offered Southern Co. and its partners $8.33 billion in federal loan guarantees in February 2010 – $3.46 billion to Georgia Power Company, $3.06 billion to Oglethorpe Power Corporation, and $1.81 billion to the Municipal Electric Authority of Georgia. Since then, the Department of Energy has extended its $8.33 billion loan guarantee offer multiple times. The most recent deal between DOE and project partners was reached in January 2014, when the offer was extended until February 28, 2014.

- In April 2010, Southern Company and its partners requested a 30-day extension to deliberate and by June they accepted DOE’s offer. The deal was valid until 90 days after the Nuclear Regulatory Commission awarded Southern Company and its projects partner a combined construction and operation license (COL). Yet, once the project received its COL from the NRC in February 2012, DOE and Southern Company announced a second extension until December 2012. As 90-day deadline approached, DOE and Southern Company once again extended the deadline for agreement on final loan guarantee terms until June 2013.

- In late June 2013, more than three and a half years after the initial offer was made, DOE and Southern Company quietly agreed to a fourth extension until September 30, 2013. A fifth extension was then awarded that set a new deadline of December 31, 2013. On New Year’s Eve, the deadline was pushed to January 31, 2014 for Southern Company and Oglethorpe Power, while the offer for MEAG was extended until July 31, 2014. Most recently, a seventh extension was made to the offer setting a new deadline of February 28, 2014.

- Documents obtained through the Freedom of Information Act after years of effort reveal wide-ranging negotiations between the Office of Management and Budget, Department of Treasury, and the Department of Energy on what the appropriate credit subsidy cost[4] should be. Years of closed door negotiations have likely allowed loan guarantee partners to craft a deal that heavily benefits them and exposes taxpayers to even greater risk.

Southern Spends Big Lobby Dollars

- Southern Company has spent far more than any other electric utility on lobbying the federal government. In 2013, it spent $12.85 million or roughly $35,000 a day, in order to help strong arm a favorable loan guarantee deal when their financials and the project all point to a bad investment for taxpayers.

Taxpayers Will Lose

- High costs, construction delays, and technical problems have plagued the nuclear industry since its inception. The Vogtle project is on the same trajectory with multiple delays and technical problems.

- Private rating agencies are reacting to the rising costs and risk of the Votgle project; the federal government should follow suit.

- Increasing competition from other energy sources such as natural gas has already led to many proposed reactor projects being delayed or cancelled.

- Even in the heyday of lending on Wall Street, private backers were not interested in investing in new nuclear reactors because of their massive financial and technical uncertainties.

Putting the full faith and credit of the U.S. government

behind this costly, high-risk project is fiscally irresponsible.

For more information, please contact Autumn Hanna at (202) 546-8500 x112

or autumn [at] taxpayer.net

APPENDIX ONE: COMPANY PROFILES

Southern Company

The Atlanta based Southern Company was created in 1946 but descends from holding companies dating back to 1912. The energy conglomerate has eight subsidiaries which have a combined generating capacity of 46,000 MW and serve 4.4 million customers in Mississippi, Alabama, Georgia, and Florida. Southern Company constructed nuclear reactors 1 & 2 at its Plant Vogtle in the 1980s after selling 30 percent of their generating output to Oglethorpe Power and 17.7 percent to MEAG in 1976. The initial cost estimate of constructing those two reactors was $660 million, but the project’s final cost was $8.87 billion. The energy conglomerate currently has around $1.8 billion in outstanding debt and a debt-to-asset ratio of 35.72 percent, more than the utilities industry average.

Georgia Power Company

The utility was formed in 1883 by Atlanta citizens but acquired its name after becoming part of a Southeastern Power & Light Company, Southern Company’s ancestor, in 1926. The company, now based in Birmingham, Alabama serves over 2.3 million customers and had a net income of $1.17 billion in 2012. Georgia Power has a 45.7 percent stake in Vogtle reactors 3&4 and though its share of the costs of constructing the units was originally certified at $6.11 billion, the company reported in February, 2013 that its share had increased to $6.85 billion. Georgia Power is currently financing the costs of the Vogtle project in part by charging its customers in advance with a tariff referred to as a Nuclear Construction Cost Recovery Rider with a Construction Work in Progress (CWIP) balance that totaled $2.65 billion at the end of November, 2013.

Oglethorpe Power Company

The company, now headquartered in Tucker, Georgia was founded in August 1974 by 38 municipal electric cooperatives that wanted to end their reliance on Georgia Power Company for wholesale power. Oglethorpe Power and its 38 ‘Electric Membership Corporations’ provide electricity to 4.1 million people in 151 of Georgia’s 159 counties. In its 2012 annual report, Oglethorpe reported that its share of the Vogtle project’s costs (30 percent) had increased from $4.2 billion to $4.5 billion. That $300 million and any further cost increases might be difficult to finance for the company that had a 2012 net income of $39.6 million. The DOE loan guarantee would allow Oglethorpe to cover $3.06 billion of its share of the Vogtle costs with debt though the company had originally planned to only borrow $2.2 billion from capital markets.

Municipal Electric Authority of Georgia (MEAG)

MEAG Power, a not-for-profit public energy consortium based in Fulton County, Georgia, was created by the Georgia General Assembly in 1975 to provide power to small cities and towns. Since then, 49 communities throughout the state have joined the public corporation. MEAG estimates its share of Vogtle reactors 3&4 construction costs (22.7 percent) will come to $4.2 billion. To finance that amount, MEAG has issued three series of bonds since 2009: Project M bonds, Project J bonds, and Project P bonds. The three Projects represent a certain percent of MEAG’s share of the reactors’ expected output. The communities in the consortium have agreed to buy their power from one of the Projects and in turn are obligated to bear the financing costs of Vogtle construction. Further increases to the reactors’ cost will cause small Georgia municipalities to dig deeper for funds. MEAG Power had $5.7 billion in long-term debt at the end of the third quarter of 2013.

MEAG was able to designate its three series of bonds as “Build America Bonds” under the Recovery Act of 2009. As such, MEAG is entitled to receive cash subsidy payments from the U.S. Treasury that will cover 35% of the interest the company will pay to bond holders. That means that even if MEAG does no receive a DOE loan guarantee, taxpayers will still be partly subsidizing the construction of Vogtle Units 3&4.

[1] A loan guarantee is an agreement by the DOE to cover the repayment of a loan, in this case from the Federal Financing Bank to the Vogtle partners, if the borrowers default.

[2] See “Loan Guarantee Going to Unstable Partners” below.

[3] Georgia Power Company (subsidiary of the Southern Company) (45.7%); Oglethorpe Power Corporation (30%); Municipal Electric Authority of Georgia (22.7%); The City of Dalton, Georgia (1.6%).

[4] The credits subsidy cost represents that cost of the loan guarantee to the federal government. If the price is too low, taxpayers could lose big if a project defaults.