From 2015 through 2024, federal oil and natural gas production in New Mexico generated extraordinary economic value. But because federal royalty rates were set below market for most of that period, taxpayers did not receive the full value of revenues generated from those publicly owned resources.

If federal leases in New Mexico had carried an 18.75 percent royalty rate instead of the 12.5 and 16.67 percent rates that governed most of the last decade, royalty collections would have been $13.9 billion higher. Since roughly half of federal royalties are returned to producing states, nearly $7 billion of those additional dollars would have flowed directly to New Mexico—funding that could otherwise be used to support schools, hospitals, and other state infrastructure.

This is not a projection of future production. The oil was produced. The gas was sold. The only difference was how much of that value was returned to federal taxpayers and New Mexicans rather than remaining with operators.

New Mexico sits at the center of federal oil and gas production. Over the last decade, it has consistently been the largest producer of federal oil and, in recent years, the largest or second-largest producer of federal gas. Lease sales in New Mexico have always been among the most competitive in the country. In 2025 alone, nearly all offered acreage in New Mexico received bids and the average bid per acre was higher than the average in all other states.

That production strength brings real economic value for New Mexicans. Federal oil and gas revenue is shared with the state, helping fund public schools, roads, and other state and local priorities. When federal policy undervalues those resources, New Mexico does not just lose abstract federal dollars. It loses revenue that would otherwise flow directly into the state budget.

Oil and Gas Production in New Mexico

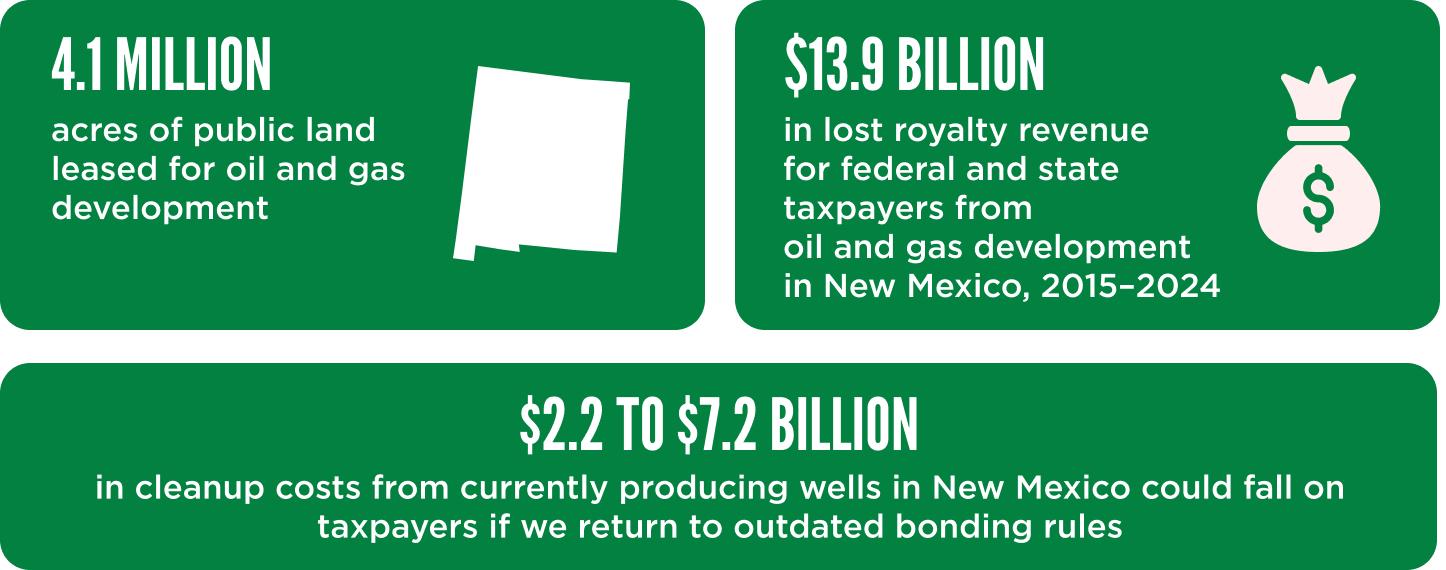

At the end of Fiscal Year (FY) 2025, 4.1 million acres of federal land in New Mexico were leased for oil and gas development.[1] New Mexico is the largest producer of federal oil and second largest producer of federal gas, accounting for 66 percent of all oil and 36 percent of all gas produced on federal lands from FY2015 to FY2024[2] Oil production on federal lands in the state has increased by nearly 5 times over the last decade and gas production has nearly doubled.[3]

This production of oil and gas should have generated even more sizeable revenues for federal and New Mexico taxpayers alike, since revenue from royalties and other leasing terms are shared with the state. However, outdated and below-market leasing terms not only limited much-needed revenue for taxpayers, but allowed oil and gas operators to skirt the responsibilities of reclaiming (cleaning up) well sites after operations cease, leaving taxpayers to cover the costs.

The Federal Oil and Gas Leasing Program

Federal taxpayers own mineral resources across the United States, including a 700-million-acre onshore subsurface mineral estate. The Bureau of Land Management (BLM), within the Department of the Interior (DOI), oversees the subsurface mineral estate and is charged with managing the development of mineral resources. Yet, despite the massive value of taxpayer-owned resources extracted from federal lands by oil and gas developers every year, taxpayers continue to receive pennies on the dollar due to outdated and below-market leasing terms.

Initially, DOI grants leases to the highest bidder in a live auction, with the resulting revenue termed as “bonus bid” revenue. Following this, the federal government imposes rent on leaseholders for holding the land before production commences. Once leases begin to produce oil and gas, leaseholders are charged a fixed percentage of the production’s value, known as a royalty.

In 2022, Congress made several long overdue updates to oil and gas leasing rates for the next decade, the first time since the 1980s. Under these commonsense updates, until August 2032, rental rates are raised to $3/acre for the first two years, $5/acre for years three to eight, and then no less than $15/acre for years nine and ten; and the minimum bid is raised to $10/acre. After August 2032, these rates will become the statutory minimum. While Congress also enacted other updates—including raising the onshore royalty rate to a 16.67 percent minimum, eliminating the practice of noncompetitive leasing, and creating a new expression of interest fee for entities nominating federal land for competitive lease sales—these were rescinded in 2025.

After production ends, oil and gas producers operating on federal land are required to plug their wells and clean up the surrounding sites. To guarantee that the cleanup of these potentially hazardous and environmentally harmful sites is paid for, producers must post a bond before they start drilling. If a company abandons its wells on a federal lease or goes bankrupt, the bond is forfeited and will be used to cover the reclamation expenses.

The BLM accepts two types of bond coverage: bonds for an operator’s wells on an individual lease (minimum $150,000) and bonds for all wells owned by an operator in one state (minimum $500,000). Higher bond values may be required if the operator has a history of violations, if BLM anticipates unusually high reclamation costs, or if there are other risk factors. These new requirements were implemented in June 2024 for new leases and set to phase in for existing leases over the next several years.

DOI is responsible for overseeing our valuable, taxpayer-owned mineral resources and guaranteeing taxpayers a fair return. Yet for decades taxpayers have been shortchanged. The federal onshore oil and gas leasing system must be brought into the 21st century. Recently reduced royalty rates, return of noncompetitive leasing, and threats to revert to outdated bonding rates and practices risk failing to protect taxpayers and failing to ensure a fair return from the sale of taxpayer-owned resources. Taxpayers have already lost billions of dollars as a result. Without permanent market-rate leasing terms and improved oversight, taxpayers could lose billions more and be saddled with growing long-term liabilities.

Royalty Rates and What They Mean for New Mexico

For nearly a century, the federal onshore royalty rate was fixed at 12.5 percent.[4] That rate remained in place as production in southeastern New Mexico surged and oil prices climbed. In 2022, Congress temporarily raised the rate to 16.67 percent for new leases, but lowered it back to 12.5 percent in 2025, locking in a century-old rate for decades to come.

Royalty revenue makes up the overwhelming share of federal oil and gas receipts. Over the last decade, FY2015-2024, the Office of Natural Resource Revenue (ONRR) collected $25.5 billion in royalties on oil and gas produced on federal lands in New Mexico.[5] Because revenue is split with producing states, every percentage point in the royalty rate determines how much funding reaches Santa Fe and local communities.

The federal government charges a 12.5 percent royalty rate, far below the 18.75 percent to 25 percent charged on state lands.[6] If an 18.75 percent royalty rate had been applied to the $227 billion worth of oil and gas produced on federal lands in New Mexico over the last decade, federal and state taxpayers would have received an additional $13.9 billion in revenue.[7]

An 18.75 percent rate is not unusual; it matches what New Mexico often charges on state lands. Texas, another top oil and gas producing state located in the Permian Basin, charges up to a 25 percent royalty on state lands. Development has not only continued but boomed under those terms. The record shows that competitive rates do not halt or slow down production. They determine how much of the value extracted from public land returns to the public.

New Mexico’s experience over the last decade makes this plain. Production on federal lands expanded rapidly, regardless of the royalty rate. Companies invested, drilled, and bid aggressively in competitive lease sales under both the higher 16.67 percent royalty rate and lower 12.5 percent royalty rate. The pace of development didn’t change—the public’s share of the profit did.

Competitive Leasing Does Not Depend on Discounted Terms

Recent lease sales reinforce this point. Even when the federal rate was 16.67 percent, parcels in Eddy and Lea counties—both located in the Permian Basin—drew intense competition and some of the highest bids in the country. In 2023 and 2024 onshore lease sales in New Mexico received an average bid of $26,000 per acre—nearly 20 times higher than the nationwide average of $1,400 per acre—and leased all parcels offered at auction. After the rate dropped back to 12.5 percent, New Mexico continued to lead in average bids per acre—$8,600 per acre, compared to the $1,100 per acre nationwide average—and leased nearly all offered acreage.[8]

Companies lease in New Mexico because the resource potential supports profitable production. They do not base billion-dollar investment decisions on a few percentage points of royalty difference. Lowering the rate does not create demand in marginal basins. It reduces what taxpayers receive in the most productive federal oil field in the country.

For New Mexico, the lesson is straightforward. Federal policy choices determine how much of the nation’s resource wealth returns to the public. From 2015 through 2024, those choices left $13.9 billion in additional federal royalties unrealized. With production levels as high as they are today, repeating that pattern will only exacerbate these losses.

Bonding and the Risk to State and Federal Taxpayers

New Mexico also faces significant cleanup liabilities from orphaned and inactive wells. When oil and gas operators drill on federal land, they are required to post bonds meant to ensure that wells are plugged and sites are restored once production ends. In practice, historic federal bonding requirements have often been insufficient to cover the high costs of reclamation, which leaves taxpayers to shoulder the costs of cleanup.

Reclamation costs vary by well depth, location, and age. The Bureau of Land Management estimates reclamation costs $71,000 per well nationwide.[9] In New Mexico, estimates of the average reclamation cost for a single well range from $160,000[10] to $218,400[11] per well.[12] When companies default, dissolve, or enter bankruptcy, taxpayers pay.

On state land, New Mexico’s Oil Conservation Division steps in to plug wells and restore sites, drawing from state funds and, increasingly, from federal orphaned well programs funded through the Infrastructure Investment and Jobs Act (IIJA). Federal taxpayers have already committed billions nationwide to address wells that were never fully secured by adequate bonding. Since 2022, New Mexico has received more than $55.5 million in federal orphaned well grants under the IIJA, including initial, formula, and performance-based awards, and the state remains eligible for up to $111.8 million more if funds allow.[13]

Prior to recent updates, federal bonding rules for onshore wells lagged far behind real-world reclamation costs. The Government Accountability Office reported that DOI held an average bond value of $2,122 per well in 2018, covering just 1-3 percent of the estimated cost of plugging orphaned wells in New Mexico.[14] In 2023, DOI reported there were 1,500 bonds covering approximately 110,000 existing wells nationwide.[15] Average coverage varied depending on the bond type, with a high of $5,864 per well on statewide leases and a low of just $671 per well on nationwide leases.[16] Combined, each existing well had an average bond coverage of $3,873, covering just 2-5 percent of the estimated cost of plugging orphaned wells in New Mexico.

Fortunately for taxpayers, federal bonding requirements were updated in 2024 and the average per-well bond coverage is expected to rise. But if updates are rolled back to the same inadequate standards as before, taxpayers could be on the hook for billions in future reclamation liabilities from currently producing wells. According to BLM, there were 33,400 oil and gas wells producing on federal lands in New Mexico at the end of FY2024.[17] If the same weak bonding requirements were once again imposed—leaving DOI to hold an average bond value of $3,873per well, like they did in 2023—the federal government would only have $129 million in financial assurances for currently producing wells that may cost between $2.4 and $7.3 billion to reclaim, leaving taxpayers with billions in potential future liabilities.[18]

For New Mexicans, weak federal leasing terms create a double exposure. First, below market royalty rates reduce the revenue flowing to the state from production. Second, insufficient bonding increases the likelihood that cleanup costs will land on state and federal taxpayers. Communities that host drilling activities will face the long-term environmental and fiscal consequences when wells are left behind and the bills come due.

What Federal Decisions Mean for New Mexico

New Mexico demonstrates that federal oil and gas leasing can generate substantial revenue when parcels are competitively offered in areas with strong production potential. It also shows how federal policy choices determine whether that revenue reflects fair market value.

When Congress reduces royalty rates, reinstates noncompetitive leasing, or delays bonding updates, those decisions are not abstract. They shape how much revenue flows to Santa Fe, how much risk sits on the state’s balance sheet, and whether taxpayers are left to fund cleanup costs decades from now.

New Mexico’s production will likely remain strong. The question is whether federal policy will ensure that the public receives a fair return for those resources. For a state that produces more federal oil and gas than any other, the stakes of getting that answer right are measurable and immediate.

[1] Bureau of Land Management (BLM), Oil and Gas Statistics, Fiscal Year 2025 Statistics. https://www.blm.gov/programs-energy-and-minerals-oil-and-gas-oil-and-gas-statistics

[2] Office of Natural Resources Revenue (ONRR), Query Data, accessed February 2026. https://onrr.gov/

[3] ONRR, Query Data, accessed February 2026. https://onrr.gov/

[4] Nearly all leases were issued at the statutory minimum royalty rate of 12.5%.

[5] ONRR, Query Data, accessed February 2026. https://onrr.gov/

[6] New Mexico Legislature, “SB 23 Oil and Gas Royalty Rate Changes,” April 2025. https://www.nmlegis.gov/Sessions/25%20Regular/ final/SB0023.pdf

[7] Taxpayers for Common Sense (TCS) calculation applies an 18.75% royalty rate to the reported sales value, less allowances, as reported by ONRR.

[8] TCS, “Federal Onshore Oil & Gas Leasing: 2025 Year in Review,” January 21, 2026. https://www.taxpayer.net/energy-natural-resources/federal-onshore-oil-gas-leasing-2025-year-in-review/

[9] BLM, “Fluid Mineral Leases and Leasing Process,” Federal Register, July 2023. https://www.federalregister.gov/documents/2023/07/24/2023-14287/fluid-mineral-leases-and-leasing-process#p-82

[10] New Mexico Energy, Minerals and Natural Resources Department, “Orphan Well Plugging & Site Remediation Update and Overview of Financial Assurance Requirements,” December 1, 2023. http://nmlegis.gov/handouts/RHMC%20120123%20Item%202%20EMNRD%20OCD%20-%20Orphan%20Well%20&%20Financial%20Assurance.pdf

[11] CAR, “An Analysis of the Adequacy of Financial Assurance Requirements for Oil and Gas Infrastructure Located on State Trust and Private Lands in New Mexico,” April 30, 2021. https://centerforappliedresearch.com/PubRep/NM_Assurance_Assessment.pdf

[12] Other estimates include LFC reporting of fiscal year (FY) 2024 OCD plugging costs of $163,000, OCD estimate to plug 1,741 orphaned wells (2021) of $166,922, Center for Applied Research (CAR) estimate for gas wells on state trust land of $168,900, OCD recent average plugging costs of $180,000, per its 2024 Phase 2 Work Plan Proposal, which are all within this range.

[13] LFC, “Policy Spotlight: Orphaned Wells,” June 24, 2025. https://www.nmlegis.gov/handouts/ALFC%20062425%20Item%204%20Policy%20Spotlight%20Orphaned% 20Wells.pdf

[14] Government Accountability Office, “Oil and Gas: Bureau of Land Management Should Address Risks from Insufficient Bonds to Reclaim Wells,” September 18, 2019. https://www.gao.gov/products/gao-19-615

[15] BLM, “Fluid Mineral Leases and Leasing Process,” July 24, 2023. https://www.federalregister.gov/documents/2023/07/24/2023-14287/fluid-mineral-leases-and-leasing-process

[16] TCS calculation divides the average bond amount per bond type by the average number of wells per bond type, as reported in the BLM proposed “Fluid Mineral Leases and Leasing Process” rule.

[17] BLM, Oil and Gas Statistics, Fiscal Year 2024 Statistics. https://www.blm.gov/programs-energy-and-minerals-oil-and-gas-oil-and-gas-statistics

[18] TCS calculation multiples the number of producing wells in the state (33,400) by the estimated cost of reclamation ($160,000 to $218,400) less the average bond value per well held by DOI in 2023 ($4,436.25).

- Adobe Stock